For more crucial details, have a look at the FHA's lending limits in your state. Generally, FHA home loans come with an extra insurance coverage charge called a "mortgage insurance premium." Because FHA loans are ubiquitous and have lower down payment and credit history requirements, they are one of the most available mortgage.

Additionally, FHA loans enable a non-occupant co-signer (as long as they're a relative) to help customers qualify. Historically, the requirements for FHA home loan insurance coverage have actually differed for many years. Presently, an FHA loan requires both an up-front home mortgage insurance premium (which can be financed into your loan amount) and monthly mortgage insurance coverage.

The U.S. Department of Veteran Affairs supplies loan services to members and veterans of the U.S. military and their families. If you are eligible , you might certify for a home mortgage that requires no down payment or monthly mortgage insurance. VA home mortgages are designed to assist veterans acquire houses without any down payment.

Comparable to FHA loans, the federal government doesn't straight issue these loans, instead they are processed by banks or private lenders and ensured by the VA - how do reverse mortgages work in utah. While VA loans are appealing due to the fact that they normally need no deposit, they do not have an optimum limitation, depending upon eligibility. Veterans, active-duty service members, and surviving partners are qualified for VA home loan.

How Does Bank Know You Have Mutiple Fha Mortgages Fundamentals Explained

These loans are excellent to get people in houses, but are just readily available to veterans. FHA 203k loans are home remodelling loans for "fixer-upper" homes, assisting property owners fund both the purchase of a house and the cost of its rehab through a single mortgage. Current property owners can likewise get approved for an FHA 203k loan to fund the rehabilitation of their existing house.

5% down. An FHA 203k loan does not need the space to be presently how do you get rid of your timeshare livable and it has credit report requirements comparable to regular FHA loans, nevertheless some loan providers may need a minimum credit report of 620 to qualify. how is the compounding period on most mortgages calculated. Lots of kinds of remodellings can be covered under an FHA 203k loan: structural repair work or changes, modernization, removal of health and wellness threats, replacing roofings and floors, and making energy preservation enhancements, to call a few.

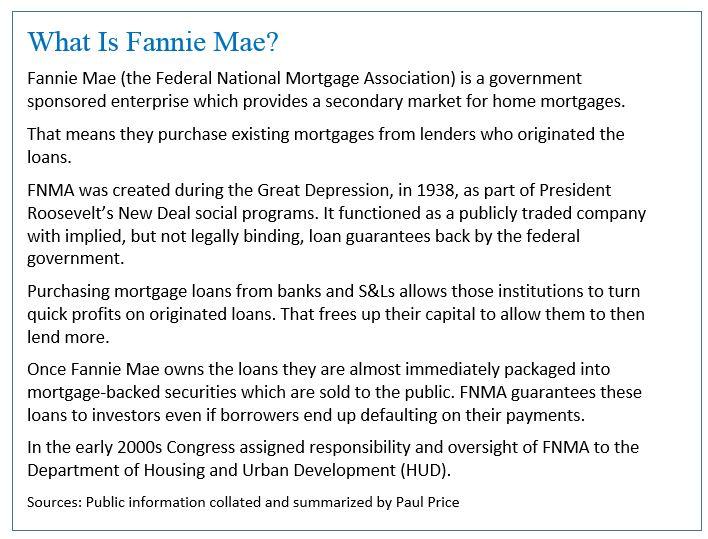

And they only need a 3. 5% down payment. how did clinton allow blacks to get mortgages easier. These loans need you to receive the worth of the residential or commercial property plus the expenses of any organized remodellings. Both adhering and non-conforming home mortgages are types of conventional home mortgages. An adhering loan satisfies certain standards established by the Federal Real Estate Finance Company (FHFA) and Fannie Mae and Freddie Mac, but they are not insured by the government.

Since 2020, the conforming loan limitation is $510,400 in the majority of the U.S. and goes up to $765,600 in certain higher-cost locations, and is changed each year. Conforming loans use better rates of interest and lower charges than non-conforming loans. Conforming loans might have lower interest rates and costs than non-conforming loans.

Excitement About Hawaii Reverse Mortgages When The Owner Dies

Non-conforming loans are loans that fall above the conforming loan limitation set by the FHFA. There are a number of various types of non-conforming loans. The most common is a jumbo loan. A jumbo loan is a loan that exceeds the adhering loan limitation. Due to the size of the loan, the requirements to qualify are more rigid.

Interest rates can also be greater for jumbo loans because they are considered more dangerous to the loan provider. Other types of non-conforming loans exist for debtors with credit rating on the lower end, or debtors with a high debt-to-income ratio. Those wanting to fund an expensive residential or commercial property purchase will likely have little choice however to utilize a jumbo loan.

Jumbo loans can assist qualified customers purchase expensive homes. Certifying for a jumbo loan might have more stringent requirements or additional fees. Each property buyer is special, so putting in the time to fully comprehend the process of picking the right mortgage for your requirements is a critical initial step. All set to do some contrast shopping? SoFi provides home mortgages with competitive rates, a quick and easy application, and no surprise charges.

SoFi Home Loans are not offered in all states. See SoFi. com/eligibility for more details. Many elements impact your credit history and the rates of interest you might get. SoFi is not a Credit Repair Company as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not offer "credit repair work" services or recommendations or assistance relating to "rebuilding" or "improving" your credit record, credit report, or credit rating.

Facts About What Were The Regulatory Consequences Of Bundling Mortgages Uncovered

The info and analysis supplied through hyperlinks to third celebration sites, while believed to be precise, can not be ensured by SoFi. Links are attended to informational functions and must not be considered as an endorsement. SoFi loans are originated by SoFi Browse around this site Loaning Corp (dba SoFi), a lending institution certified by the Department of Financial Defense and Innovation under the California Financing Law, license # 6054612; NMLS # 1121636 .

Buying a home is probably the most important purchase that you'll ever make, which is why it is essential to make the right decision. Offered the high expenses of a real estate purchase, the chances are that you will require to secure a house mortgage loan. While the standard facility of all home loans is the very same (you'll be using your brand-new residential or commercial property as collateral for a loan that allows you to acquire the property), there are various choices at hand.

No two people are the same, specifically when it comes to purchasing a house. As such, banks and lending institutions offer different home mortgage products in order to serve the different requirements of a diverse market. Understanding the finer information of the contrasting mortgage types eventually enables you to pick the most suitable path for buying your home.

Residential or commercial property rate The best home loan for a $100,000 loan might not be the best choice for a $1,000,000 mortgage. Loan-to-Value ratio When the deposit is a significant portion (over 50%) of the home price, a specific home loan type might be much better. Debt-to-Income ratio Banks factor in your other financial obligations versus your incomes to make sure that you can making payments and your scenario can influence which https://blogfreely.net/regais21pe/if-your-policy-includes-a-percentage-deductible-for-wind-hail-or-cyclone choice is best.

Fascination About Mortgages Or Corporate Bonds Which Has Higher Credit Risk

Credit history Credit rating are another influential aspect that can impact the general repayment structure. Other factors, such as the period of the home loan, will also affect the circumstance. By understanding the different home loan, it's possible to discover an option that suits your budget plan and scenario to produce the lowest total repayment.

After all, the contrasts in between one lender and the next can be huge. Nonetheless, the home loan type will constantly supply the structure for making the ideal choice. While there are other home mortgage types readily available, particularly if you're wanting to end up being a financier or landlord, home mortgage are broken into seven main categories.

It is an agreement in which your payments and rate of interest are set at a guaranteed level throughout the period of the loan. This makes the monetary management elements of the home mortgage loan far simpler to control. The term of the contract can be individualized to fit private requirements based on monetary status and personal choice.